I read Jeffrey Alhambra's recent post on Real Clear Markets about his views of the creeping inaccuracy of economic language with great interest. Sure, it was at times a hyperbolic piece, but his data points on the revenue contractions of some large companies like GE and IBM were well taken and lead me to ask:

Are there some sectors of the economy which are still in recession?

So, yes, this post will mainly concentrate on sectors and be especially interesting to ETF and mutual fund sector investors... but investors of all stripes should internalize some of these concepts.

Sales and Revenue Contraction

Anyone reading this with an MBA (or, really, any keen observers of business practices) knows that for an individual company contracting or stagnating revenue isn't necessarily a bad thing. Especially with things like consumer luxuries and technologies, it just doesn't make sense for large companies to chase revenues in every corner of the market.

Conclude with me: luxury brands don't need to compete with the cheapest of imports.

For sector comparisons, on the other hand, you better have a better conclusion. Is revenue leaking overseas? To new, smaller upstarts or private firms? Your answer makes a difference - this data comes directly from S&P and encompasses the 500 stocks which S&P chose to include in the index at the time.

Let's get down to it.

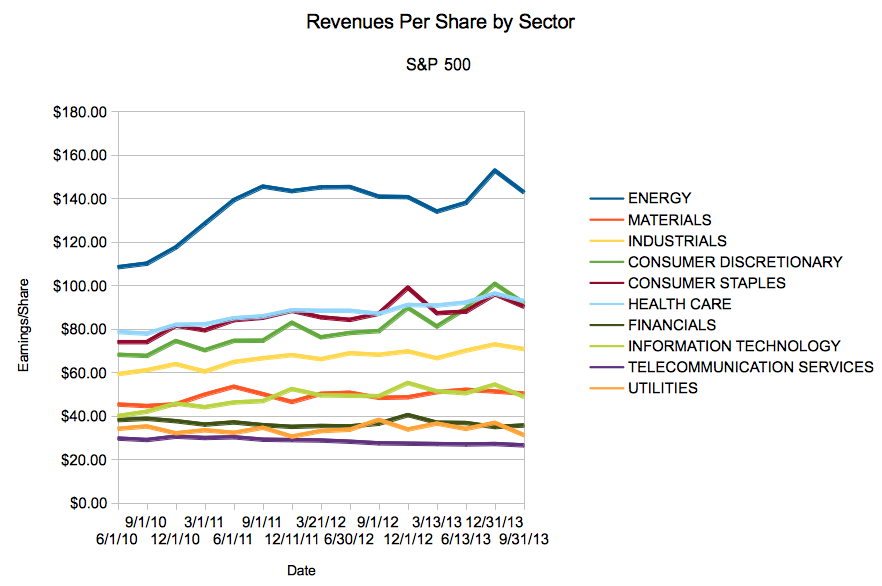

Revenues per Share in S&P 500 Sectors, since Q2 2010

So... lots of stuff going on here, but we think these are the important points:

- You've got some obvious high flyers, like Energy and Consumer Discretionary.

- You've got some obvious stragglers, like Telecom, Utilities and Financials

And yes, I would have gone back further if I had the data (or if someone gave me a subscription to something like Morningstar or CapitalIQ, thanks in advance).

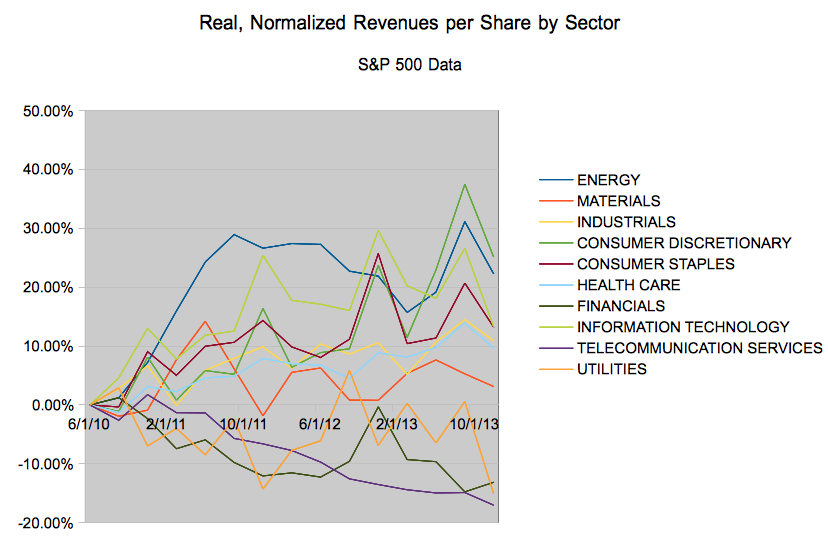

A Better View of the Trend!

In the interest of tired eyes and fingers itchy to hit a back button, let's clean up our data a bit and try to figure out exactly what we should be measuring. We can't really strip out seasonal trends since our sample is too small, but we can do some important things:

- We can adjust for inflation (CPI-U SA, I asked FRED to average it quarterly. Make an argument for non-adjusted, perhaps?).

- We can normalize for Q2-2010 by setting that as our baseline (0%), and returning the absolute change from that point

So, no, no annualized changes in revenues or anything.

Here's the much more interesting chart we get when we apply said adjustments:

Your Take?

Your Take?

So, yes friends, this might be a story about pricing power - tech, energy, and consumer discretionary have been able to push their revenues up from 2010. Other sectors? Not so much.

Okay, let's open it up to audience participation, because the players we called out earlier have obviously contracted in revenue (but not necessarily in margins - but we'll save that analysis)... and materials haven't fared to well either.

Full disclosure: I own VAW, the Vanguard Materials ETF. I don't own GE or IBM. And, yeah, I've got plenty of S&P 500 in one form or another - but I'd be pretty flattered if that moved the market.