We try to wear our brains on our sleeves (I should trademark that) when it comes to some of the innovations we've rolled out on the site. If you check out our Calculators and Visualizations page, we've got everything from historic S&P returns to predictions of how noise levels affect real estate values. However, one of our favorite series has been the 'Predicting the S&P 500' series, which we brought back Monday.

Why, if we liked the series so much, did we stop doing it in August of last year? Well, in a word, the results have sucked. That's actually the scientific word that describes the results of the experiment. However, just like a real experiment in a hard science, the failure actually reveals something interesting - interesting enough that we want to bring this series back. Not for irony or glory or to steer you wrong, mind you - but as an example of a weird little trick of options markets. And hey, if you're paying attention, you might even be able to exploit it.

Failing in the Same Way

When we set up our options prediction calculator, we designed it to try to predict 75% of closing prices using the relative prices of puts and calls. Specifically, the 75% range is supposed to be the middle - when predictions break down, 12.5% of the time they should have been too optimistic, and the other 12.5% of the time too pessimistic. I've also been tracking the 50 percentile/median - roughly the breakeven point on a future contract.

Our results? (Click to see it all in a tidy spreadsheet)

For calls, 13 out of 29 predictions came to fruition, or 44.83%. Worse than a coinflip!

For puts, 6 out of 29 predictions came true - 20.69%. That's right - worse than 100 - implied probability.

So, It Didn't Work. Why Share Your Shame?

Ahh - but like I implied earlier, it doesn't take a success to be a valuable experiment. When digging into the numbers, you'll notice something weird - not only did the predictions fail to pan out a majority of the time, most of the fails were in a single direction - too pessimistic. That's a huge deal, if you consider the implications. This model is based on the pricing of contracts - so in 2012 I've got a log of mis-priced options contracts (assuming either direction, magnitude or time-frame was foreseeable). In 2012, anyone who believed the predictions were too pessimistic - especially the predictions in puts contracts - would have made out like a bandit.

Now, what's behind the failure? It's easy to look at a year and say it was somehow an outlier - that, perhaps, markets were rational, and a whale like the Fed forced the hand of the larger market. Perhaps it was a complete fluke, and there was no reason for the pessimism. Perhaps the slight pessimism itself is a feature of the options market, which is again pervasive in pricing for this year. Or, and I personally think this is the most likely scenario, traders don't want to shake the tree too much - so if you have a good bead on the market's direction, up or down, over the next year, you can look at where the pricing falls and perhaps beat the game.

Yesterday, the S&P 500 ETF SPY closed at 145.92 (The S&P 500 closed at 1,461.02, but we've been tracking SPY technically). Calls seemed (remember, I pulled the numbers last weekend) to be pricing the 75 percentile close range on January 17, 2014 at 145.1 and 157.0, while puts claim between 118.2 and 143.2. Here's Yahoo's quotes on Jan-14 SPY contracts. Think you can take advantage of the market's claim?

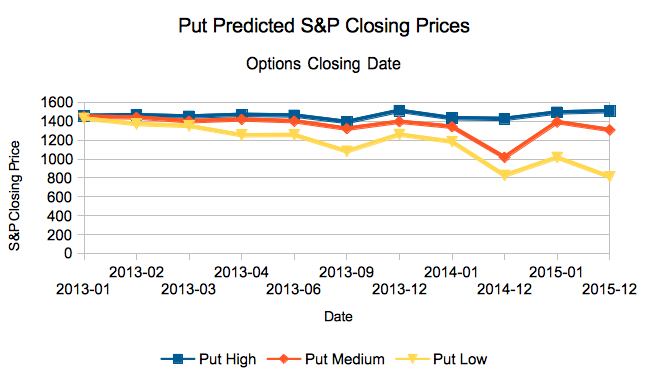

Here's the chart of interest to you sharks, SPY puts:

Go get them!