I love Canada.

I say that without a hint of sarcasm. I speak for a majority of Americans here - jokes about hockey, curling, and freezing temperatures aside, we really do want Canada to succeed.

Your neighbors to the south (The United States) recently went through some incredibly hard times in our real estate market - our real estate crash was quite difficult, and even today, in an environment of increasing home values, our prices are still 25% below the peak seven years back.

That's why we read our friend Nelson's (of Financial Uproar fame) post on the coming Canadian real estate crash and became increasingly nervous.

This Time It's Different (The Canadian Real Estate Edition!)

Dow 40,000 anyone?

The phrase "this time it's different" was finally converted to book title form in 2009, when [amazon-product text="Carmen Reinhart and Kenneth Rogoff" type="text"]0691152640[/amazon-product] wrote the eponymous book about bubbles over the previous 8 centuries. (Yes, that Reinhart and Rogoff!). They, of course, didn't coin the phrase - but the fact that it's now immortalized in a book title doesn't change the common thread running through every single example - the exhortation to buy now (or be priced out!). Anyone who tried to dismiss asset prices running away from fundamentals would be told "this time is different - the game has changed" or "the fundamentals don't matter".

Well, Canadians may think that "this time is different", but, speaking from the perspective of someone alive during 2005 in the United States (and a person deeply obsessed with teasing important data out of large data-sets!) allow me to state:

Canada, your current real estate statistics are even worse than the US at the 2006 peak.

Seriously - you'll get a kick out of this September 2005 report on housing and the mortgage markets by the Mortgage Bankers Association.

Now read this list of Canadian articles. (Or trust me: the summary: "this time it's different!").

Growing Signs of Mania in Real Estate Purchases

Yes, we get it - the plural of anecdotes is not 'data'. When you accidentally come across a lot of people behaving in a similar manner, there is usually some selection bias at hand.

Still, a large number of our Canadian blogger friends have recently purchased real estate - condos, town homes, and single family homes. We imagine that the personal finance-sphere tends to be more conservative financially than the rest of Canada... so, at risk of losing all credibility in the anecdote/data wars - we feel that conservative personal finance types diving headfirst into a rapidly appreciating market doesn't bode well for the market in general.

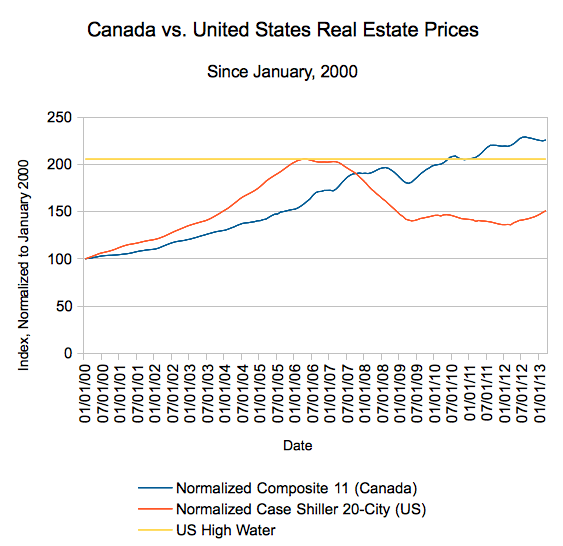

'Mania' though? Again, I'm not Canadian (that's a lie - I have distant roots in Newfoundland!). All I can do is show you Canadian real estate stacked up against United States real estate of recent vintage. Here's that mania I was talking about (both indices have been normalized to January 2000 = 100, so '200' means 'doubled in price'). Pay attention to the yellow line - that's the maximum 2000-relative level American real estate hit.

Sources: Case-Shiller Seasonally Adjusted 20 City Composite from St. Louis Fed, Teranet 11 City Composite from Teranet and National Bank of Canada

For the record, the American high water mark was set in May 2006, at 205.4577 (105% increase from Jan 2000). As of March, Canada is at 225.6550.

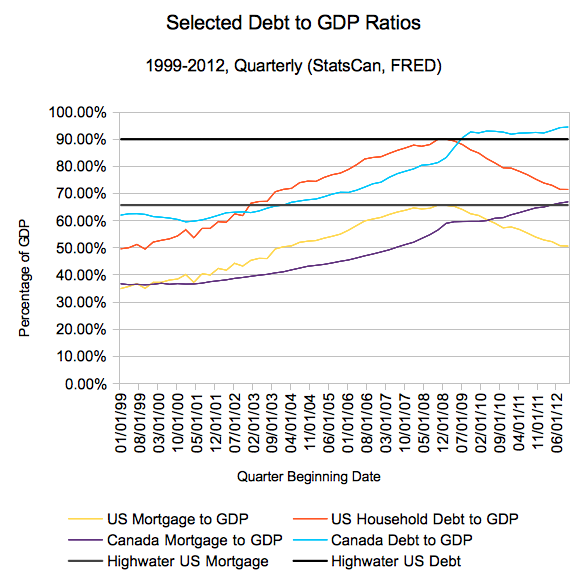

The Most Important Chart You'll View Today - Consumer Debt vs. GDP in Canada and the United States

Yes, I get the knock on the United States - we stretched too far with our debt loads, and we bought way more house than we could afford. I mean, we should have seen it coming... right?

For the record, we agree 100% with that assessment - and the United States has de-leveraged quite a bit since the bubble burst 7 years ago. So, Canada - you're right. The United States was stretched too far, and we did have it coming.

So, can that teach us anything about Canada? Well, not as simply as you would expect, unfortunately. Using a combination of Statistics Canada data and US Data we pulled from FRED, we were able to synthesize some very interesting data on consumer debt as a percentage of GDP. (If there was an easier way, please let your friend PK know!).

Since it took us 35 minutes to put it together, we've packaged it here to make your own number crunching more efficient: consumer_debt_to_gdp_us_canada

Sources: The US data is pretty straight forward, grab it from the New York Federal Reserve. GDP can be found on FRED. To make the Canada data, get GDP from Stats Canada, and get household debt to GDP. For consumer mortgage debt, get that from this Statistics Canada table.

Again, note that I have plotted the US high water marks, in dark grey and black. Note that Canada has blown through the worst excesses of the United States. Finally... note how quickly the de-leveraging occurred to bring US debt ratios back to 2003/2004 levels.

Here are the highlights:

- US High Water Household Debt to GDP: 89.99%

- US High Water Household Mortgage Debt to GDP: 65.74%

- Q4 2012 Canada Household Debt to GDP: 94.49%

- Q4 2012 Canada Household Mortgage Debt to GDP: 66.93%

I agree the US was over-leveraged. But look at those numbers - Canada has now surpassed the peak leverage ratios of the United States.

The Song Remains the Same

Been reading Don't Quit Your Day Job for a while? You probably know we're not the biggest fans of John Maynard Keynes. Still, the man is quotable!

"Markets can remain irrational a lot longer than you and I can remain solvent." - JMK

Smart quote, but what does it mean? Look at the quote by a far more famous man - Jesus, in Matthew 24:36 (hey, How I Met Your Mother did it!):

"But of that day and hour knows no man, no, not the angels of heaven, but my Father only."

When will the bubble pop? No one can give you an exact date, and the straw that breaks the Canadian camel's back can only be found in retrospect. No one can tell you how quickly it will deflate either - soft landing? Flat for years? Quick rebound?

If I knew, well... yes, I wouldn't tell you about it. Still, this looks very frothy to me (as does Bay Area Real Estate, as does the US Stock Market, but both not as bad as Canadian Real Estate). If you are exposed to Canadian real estate in any capacity, please read our friend Nelson's article.

And please be careful. This time isn't different.