This article will detail how to calculate your savings rate and emulate our method of calculating our own. We will show you savings calculations using a strict method which only includes the accumulation of assets, as well as the more typical method which also includes paydowns of debt. All our methods are after tax, also known as "net savings". All our methods are annual savings calculations, as it's a convenient (and significant enough!) time-frame in which to perform all this math.

This article, of course, comes after we recently posted our own savings rate for 2014 - a healthy 37.26% (and 46.21%, if you include principal paydown). This article details both how we arrived at those numbers, as well as explains how you can compare your own savings rate to ours.

Calculating Your Total Income

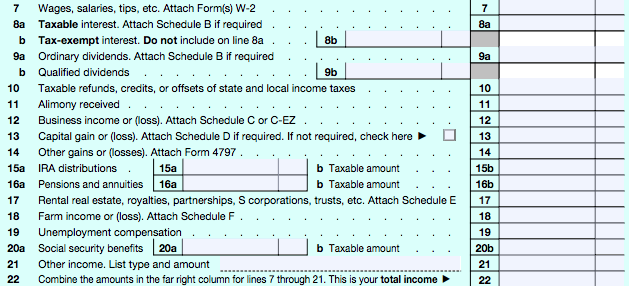

The easiest way to calculate your savings percentage - or to do any of these calculations, actually - is to do them at the same time as you do your taxes, or soon after your taxes are filed (and the pain is still fresh in your mind!). Here's a copy of the 2014 1040, which gets us most of the way to what we want to use as 'Total Income'.

The 1040 Gets Us Most of the Way to a Total Income Number

Basically, your first step is the follow the instructions on the 1040. For the majority of you, that means your biggest numbers will be from wages, salaries and tips as well as business income from a number of you. Be sure to note dividends and interest as well.

While the 1040 has you list 'Total Income' using only some of the boxes, you'll actually want to go further - include any of the 'left column' income types in your number as well, such as tax-exempt interest.

You're almost done, but not yet - and this isn't immediately obvious, but you have other forms of income which won't show up here. Specifically, for our readership, that income takes the form of traditional 401(k) contributions, 401(k) matches from your company, HSA contributions, and deferred compensation plans. I won't pretend to know every form of income which sidesteps the form, but if you've got it, make sure you add it to your own numbers.

An example:

Wages + Business Income + Interest + Dividends + 401(k) contributions + 401(k) match =

$60,000 + $10,000 + $1000 + $4000 + $2000 + $2000 = $79,000 in total income

Calculating Your Savings Percentage

'Savings' is actually a tiny bit controversial, because it may mean just accumulating assets... but from an accounting perspective principal paydowns are savings as well. We'll take you through the asset part first, as principal paydowns are just added to that number to come up with the second rate.

There is actually a fair bit of judgement calls when determining which assets are savings. You will want to include your contributions to investments and savings accounts which you generally will not be touching. That means an emergency fund which you plan to keep roughly constant counts, but the checking account which you pay all of your monthly bills from doesn't count. All of your investment accounts or purchases (such as rental property) count, because you will keep those for a while.

An example:

401(k) contributions + 401(k) match + Roth IRA + 529 + Taxable Brokerage Account =

$2000 + $2000 + $5500 + $3000 + $1200 = $11,000 in savings for the asset method

Now, to get your total for the more expansive definition of savings, add all principal paydowns. This usually means mortgage and car payments, but also includes student loans for our younger readers, as well as revolving debt such as credit cards.

An example:

Asset accumulation + mortgage pay-down + student loan pay-down =

$11,000 + $4500 + $2800 = $18,300 in total savings

(To be clear, any change in the market price doesn't count as savings - so, no, you can't count stock price increases or home price increases as savings, unless you liquidated those holdings in the previous year and it showed up in income as well. Although those are undoubtedly net worth changes, they aren't the product of active saving.

Also, I don't know where this couple lives, sorry.)

Calculating Your Total Taxes

We've settled on a definition of taxes which includes just income taxes (and payroll taxes, if you draw that distinction). That includes taxes on interest and dividends, and capital gains taxes. It also includes surcharges and any AMT.

It doesn't include our sales and property taxes (and the like - luxury taxes, various government fees, gas taxes and so on) - we assume they will stay relatively constant or increase at a steady pace, so we just include them as part of the total spending. Our argument? We're only concerned with total income in this equation, so we only include the income taxes. Seems logical, but feel free to make a case for backing out another tax if you think it muddies the rate too much.

As example (single, California, estimates):

Income Taxes + State Income Taxes + Payroll Taxes + Capital Gains Taxes =

$11,000 + $4200 + $5105 + $705 = $21,010

Calculate Your Savings Rate!

It's all gravy from now. Your net income is (Total Income - Total Taxes). For our hero, that means ($79,000 in income - $21,010 in taxes) = $57,990 in net income.

For a strict savings rate, take (strict savings amount / net income) = 18.97%

For a total savings rate, take (total savings amount / net income) = 31.56%

For effective tax rate (you may as well do it now!), take (total income taxes / total income) = 26.59%

Nice - you now know how to calculate your savings rate! And now that you have these numbers, what do you do with them? Well, compare them to your peers, of course! Here's a nice list of pieces we've created to help you do just that:

Your savings rate along with your total net worth also helps determine another interesting number - you can approximate the time when you will be financially independent. Financial independence is the ability (but not the requirement!) to retire. You can continue to work if you so choose, but that decision will be strictly optional, as your accumulated savings and spending habits will carry you.

We have an estimator (of course, see a real advisor if you need help with a decision, that calculator lacks nuance), which allows you to approximate when you'll reach financial independence. I'd suggest using your "total savings" rate, not your strict rate, in the calculator. Also, try various combinations of investment returns for different market scenarios.

So, how did you do? Did you like this primer? Where does your methodology differ? How do you calculate your savings rate?