On Monday we brought you our brief examination (anything without a calculator involved is 'brief' here on DQYDJ) of recent Nobel Prize winner Robert Shiller's cyclically adjusted P/E ratio and what it meant for today's pricing in the S&P 500.

For those of you who just found our site, you might not be familiar with Shiller's work. That's fine. Today we're going to talk about someone who I know you've heard of: Mr. Warren Buffett.

See The Finale - What Does it Mean?

From Ivory Towers to Streets Named After Parts of Homes

Robert Shiller does have some investing cred - he and his compatriot(s) Karl Case (and Allan Weiss) lent their names to the Case-Shiller home price index, a long running series of home prices in America. Shiller's CAPE (as described in the last article) also has inspired a few mutual funds, ETFs and ETNs with strategies (and a licensed title), if you look around. Still, it's safe to say that his work is a bit removed from the psyche of the average investor.

Warren Buffett on the other hand? Everyone has heard of him. Cutting his teeth as the best student in the famous Dodd-Graham courses at Columbia, he went on to investment celebrity with huge market beating margins from the 1950s(!) until today. While some might dismiss his track record as an incredible streak of lucky coin flips, others invest their faith in the man (the myth and the legend). Even rational market types find it hard to rectify their theories with the so called "Buffett effect" - the self-fulfilling prophesy of high returns which follows in the wake of a Buffett stock buy.

Buffet's Overvaluation Formula

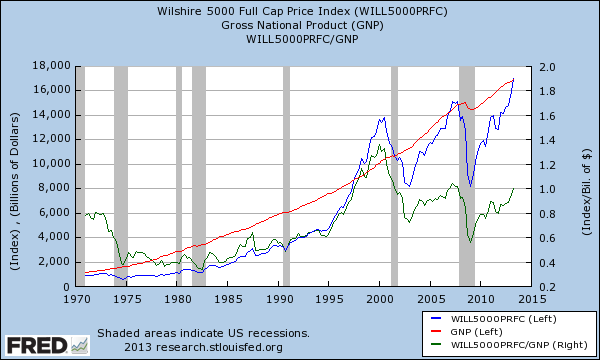

Buffett uses his own metric to decide when the stock market might be overvalued - the ratio of the total stock market's capitalization to total Gross National Product. In Buffett's original methodology, he looked at the capitalization of all companies, supposedly including private companies. We use the St. Louis Fed's Market Capitalization for the Wilshire 5000 as a proxy, along with GNP. Here's what we get:

The green line is the most important ratio - it belongs to the right axis. You can see that the ratio has crept back up to 1.0.

And what's a fair value? Luckily, we've got Buffett himself with the answer - in an Op-ed you might remember from back in October 2008 (the bottom in stocks came around March 2009 - if you listened to Buffett you would have been handsomely rewarded) when this ratio stood at 62.3% (it bottomed the next quarter at 56.3%, not seen since the recession of 1991).

It's now at 100.4%.

So It's Overpriced?

Well, just like in the last article, there are caveats... working for and against the measure:

- More foreign earnings by American companies in the last 20+ years - True, but GNP does include earnings abroad by citizens

- More private companies - this works against the index, but it is true that post-Sarbanes Oxley there are less public companies in the United States. Buffet's measure may or may not include private companies.

- Inflated earnings - this could also affect the Shiller index, but margins have increased even as unemployment has decreased leading some to theorize there is a permanent decline in competition

You can probably think of a few more, but let's be honest - we're just chasing nickels around hundred dollar bills here. As a quick glance measure, this ratio has obviously gone up quite a bit. That doesn't mean stocks will implode tomorrow - note that in 2007 it took a whole year of "over 100%" before we saw a fall, and in 2000 we got up to 133% before the decline.

What Does Buffett Say?

Before you tell me what you think in our infamous comments sections, let's listen to Mr. Buffett: "stocks are more or less fairly valued".

I guess maybe we can call the Shiller and Buffett measures "Goldilocks" methods since the proprietors both say the market is just right.

Let's try to avoid sleeping in a bear's bed.