We'll admit to being a bit bored with the markets lately - sure, we feel things are a bit heated, but we don't see any major bubbles brewing in the American equity markets like some commentators. Add that to the fact that trading volumes are low in the summer anyway, the world is fascinated with America's sixth favorite sport (okay, we kid; the Portugal-US game is on right now) and inflation has been low.

Checking In on Inflation Expectaions

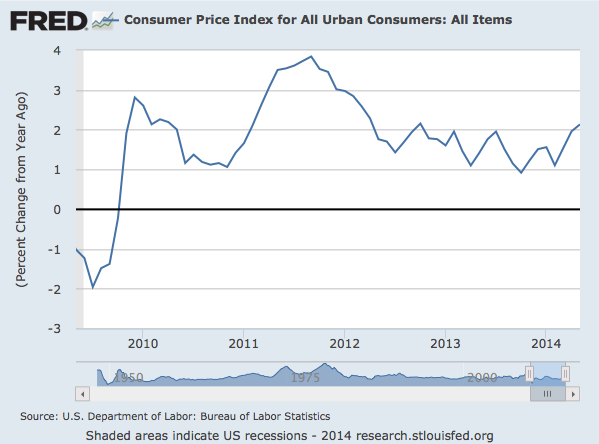

Let's kick this off with a year over year CPI Graph, straight from FRED:

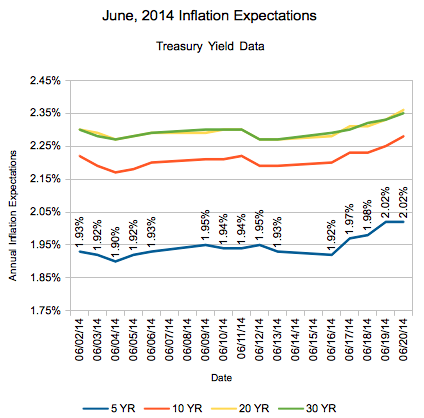

One of the things we do from time to time is check in on the market's inflation expectations. The calculation is easy - subtract the cost of inflation protected securities from Treasury yields, and you get numbers representing the market's thoughts about annualized inflation (well, CPI) over the specified time-frame. It also gives us the opportunity to make nice graphs like this:

Year to Date Inflation Expectations - June, 2014

Notice the hitch in mid April as inflation surprised to the upside. Let's zoom in a bit to take a look at that last little rise as we approach today (which really came just last week):

June 2014 Inflation Expectations

And there you have it - last week on Tuesday there was a 'sharp' increase in inflation expectations across all the time-frames we're tracking - 5, 10, 20, and 30 years.

It's Time to Watch Inflation Again!

Well, it had been low. Now, for two consecutive months the year over year inflation rate, measured by the seasonally adjusted CPI, has been at or above 2%. Now, back about 18 months ago we discussed that folks warning us about hidden or ongoing hyperinflation weren't checking the numbers - and we aren't ready to shift from that stance. However, it's time to start paying attention to the ongoing inflation rate, especially if it ticks into the upper 2s or 3s year over year, in the face of increasing wage pressure.

So, what are you seeing out there? Is it time for the last few of you to grab cheap long term debt? Is the era of 0-2% inflation over? More importantly, is it time to turn an eye back to the market... in the midst of summer?