"You are technically correct - the best kind of correct." - Bureaucrat #1, Futurama 2ACV11 - How Hermes Requisitioned His Groove Back

Editor: I updated the chart to coincide with the S&P 500 breaking the nominal closing price record on March 28, 2013. Yes, the DJIA is still at a record high - as of the 28th, you'd be up 7.5% if you invested at the peak and reinvested dividends.

We've seen an inordinate amount of attention paid in the last few weeks to a pretty goofy indicator - the Dow Jones Industrial Average.

The Dow Jones Industrial average consists of 30 subjectively picked stocks which best represent 'large, publicly owned' American stocks. Of course, the DJIA itself is a bit of an anachronism, as most of the stocks the DJIA tracks aren't actually Industrials. Furthermore, it uses a strange calculation called price weighting, an arbitrary system which gives the most weights to companies which have higher trading prices, without regard to volume or float.

Is the Dow Jones at an All Time High or Not?

My issue with the whole mess? The DJIA recently broke through its all time high price, creating lots of happiness at financial publications. Of course, the cynical amongst the financial press instantly pointed out that, adjusted for inflation, we were actually still 12% below all time Dow highs.

Exasperating, isn't it?

Well, it's time for me to come knock some heads - yes, we're at an all time high on the Dow Jones. However, we all missed the boat. By my calculations, the Dow Jones last peaked, inflation adjusted on October 9, 2007. We briefly cracked its value on October 5, 2012, and we have been in the green every day since January 11, 2013.

How Are You Calculating the Dow Jones Industrial Average Total Returns?

Elementary, my friends - first, I grab CPI-U, seasonally adjusted, from the St. Louis Federal Reserve (tabulated by the BLS). For dates before 1/1/2013, I do linear interpolation to determine a 'daily CPI'. After the 1st, I extrapolate from 11/12, 12/12, and 1/13 numbers to come up with a daily price (I did this on Saturday, March 9th - no February numbers were available yet).

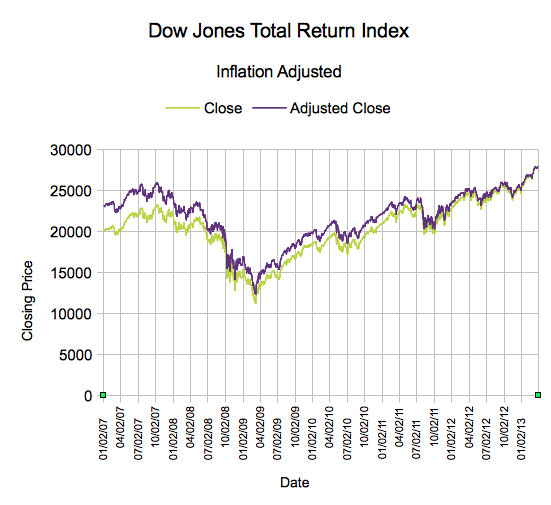

Next, I skip the Dow Jones Average. Folks, one of the hallmarks of the largest companies in the United States is they happen to have pretty decent dividend policies. That means that any reference to price returns on the Dow Jones Index is a dodge - most of you, if you are investing in the DJIA, are reinvesting your dividends. Luckily for us, dividend reinvestment is already calculated into one version of the index - enter the Dow Jones Industrial Average Total Return Index (warning: PDF).

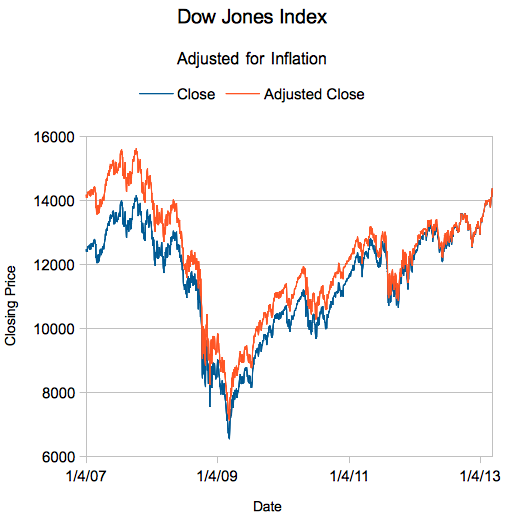

Put those together and you get that fine looking chart above. If you don't, you get this halfway there chart which only calculates the inflation adjusted closing price:

On the Importance of Being Technically Correct

It might seem like a minor point, but it's absurd to toss out dividend yields on Dow stocks. As of today, Index Arb reports the dividend yield to average 2.81% on DJIA components. I'll never understand why the financial press refuse to factor in dividends - whether received or reinvested.

I know what you're thinking - is there still a shortfall to looking at it like I'm looking at it? Yes, but it's impossible to quantify (making this analysis superior). You can't invest directly in an index, so you have to deal with transaction fees and tracking errors if you invest in a Dow Jones fund in real life (or make your own through options, futures, or other instruments). Also, depending on where you invest, you might also owe taxes - and unlike here on DQYDJ, the IRS ignores the effects of inflation for capital gains and dividends.

So, I make no apologies for being annoying on this topic - I believe if you're going to invest or look at long term returns, you need to look at the effects of reinvestment (I consider DQYDJ the gatekeeper on this - see our calculator on the S&P 500 and the 10-Year Treasury Note). Price return isn't so great of an indicator, considering that if you are in the market long enough, the effects of dividends will start to outweigh all other factors in your return.

So, join the charge - let's not let the mainstream financial press be lazy about this one, eh? If an engineer with a spreadsheet program can figure it out, so too can you, major publications!