Previously, we've discussed how important of understanding elasticities in welfare analysis. Today we're going to relate elasticities to a very important concept, tax incidence.

What is Tax Incidence?

Tax incidence is the study of who truly pays a tax.

It's best to start with an example. If a $50 tax is placed on a good – say, a washing machine – the tax incidence attempts to measure who is paying the $50.

Now, you might assume it all falls on the consumer, or if you're a contrarian all on the company. Of course, if Whirlpool could charge an extra $50 and not reduce demand, then they probably would already price their washing machines higher.

The price after-tax usually will fall somewhere between $0 and $50 higher than the original price, ceteris paribus.

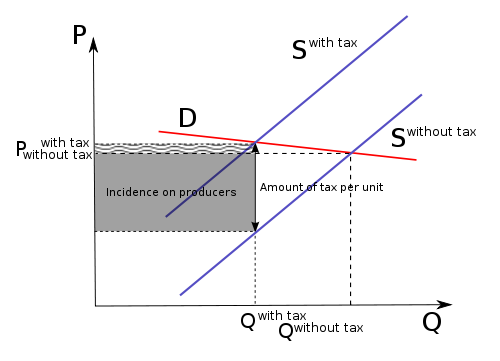

Incidence of a new washing machine tax

In this example, let’s pretend that the price after tax raises $30.

Demand for washing machines falls accordingly, and a large brunt of the incidence lies on those who still need to purchase washing machines. Think about the population this might include:

- New homeowners purchasing a house without appliances

- Shoppers looking to replace older machines

- Renters who are furnished by their landowners (who pass off the extra investment in higher rents)

- Laundromat owners

- Any number of other unintended targets

On the supply side, Whirlpool still pays for some of the tax.

Not only do they receive $20 less per washing machine sold ($50 tax - $30 price increase), they're facing decreased washing machine demand.

Logically, you can assume they'll shift their appliance production schedules accordingly.

Who might this then also affect?

- The workforce (in the form of layoffs)

- Shareholders (reduced stock price)

- Suppliers (reduced demands for factors of production, such as belts and pulleys)

As you can see, the tax incidence of a simple washing machine tax would wind its way through the entire line of investment, production, and distribution.

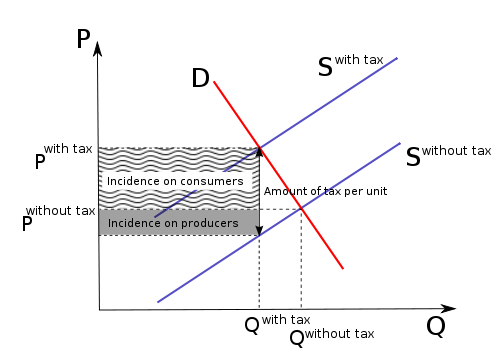

How taxes affect unintended parts of the economy

This example how various forms of taxation are felt by different levels of the economy.

But, you might ask: how do price elasticities affect tax incidence?

If the demand is extremely inelastic (say, cigarettes or life-saving medicine) the consumer gets most of the incidence. Consumers will not trade out of medicine for a worse alternative if it's a a necessity.

On the other hand, if goods with relatively elastic demands (say, fruits or cars) are taxed, consumers will explore alternatives. An apple tax might increase the demand for oranges, and a tax on cars will increase use of bikes, motorcycles and public transportation.

Tax Incidence in Politics

Tax Incidence isn't necessarily a well-explored topic in politics, but some campaigns have approached it cautiously.

Most famously, Mitt Romney declared (in response to a heckler) that "Corporations are People, my Friend!" during his 2012 Presidential campaign.

Romney's argument? The earnings of corporations eventually will be paid to a person - a corporation itself can't do anything with profits. Corporate taxes are exactly the same - they need to be paid eventually by an individual. Some combination of customers, shareholders, and employees will bear the cost of corporate taxes.

Real World Example of Unintended Tax Incidence Consequences

Let’s take a real world example now. Gas prices are a relatively inelastic good.

Consumption changes in petroleum do not match the magnitude of the price changes. Due to this, we expect tax incidence to fall largely on the consumers – drivers, primarily.

A very fungible good such as gasoline means firms cannot price differentiate. Due to the decreased demand, competition in the gasoline market will keep the prices low.

How do these two contrary effects balance each other?

This paper claims that the tax incidence of gas falls around fifty-fifty on the producers and consumers.

There are many benefits to increased gasoline taxation, mostly because gas expenditures benefit those where the incidence lies.

In other words, if you don't drive, you don't benefit from public roads as much as those who do drive. Because of this, the incidence should be on those who drive.

So, gas taxes are an example where the incidence is appropriately distributed.

Some links for analysis on the price elasticity of crude oil or petroleum: