I've seen the arguments, and – most likely – so have you. The talking heads agree you should pay off your mortgage. While a fine goal for your retirement, the vast majority of people have no need to pay off a mortgage early.

Today I'll take up the opposite argument. For most of you, don't pay off your mortgage early. Let's discuss the reasons.

1. Your House Is Not an Investment

You might think your house is an investment. It isn't.

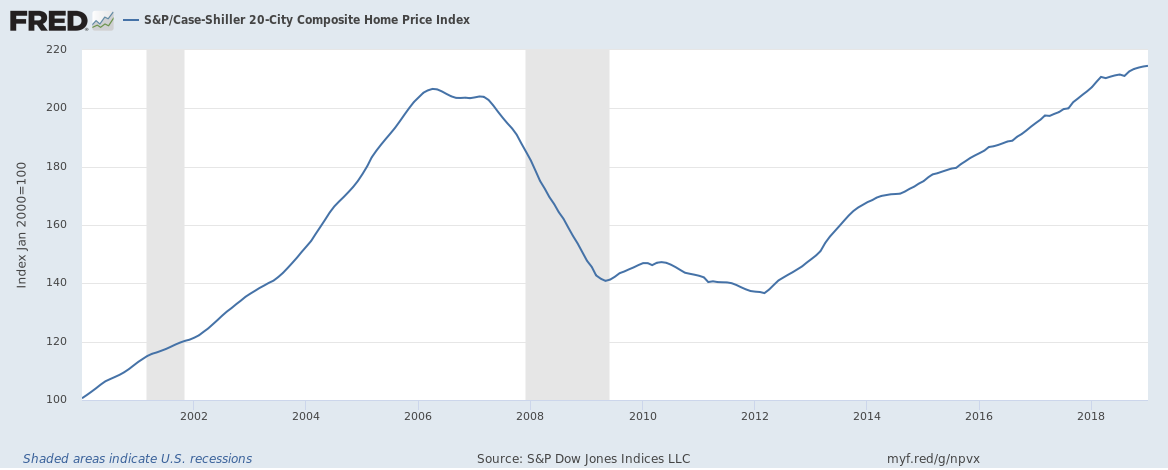

Temporarily, in a period of time roughly from 1990 until 2006, it seemed like houses were an incredible investment. That's a period we now know as a ("The") Real Estate Bubble.

13 years later we finally attained the same valuation we saw at the bubble's peak:

Sure - you can probably match inflation with your primary home. Your primary residence is a hedge against the cost of shelter. However, the idea of "Real Estate As An Investment" is new - perhaps a single generation old.

Also remember, the Case-Shiller doesn't include renovations. That's right - the structure depreciates, while your land might appreciate.

Good luck.

Here are some trailing average returns for the S&P 500 so you can compare the asset classes.

So remember, your house is not an investment: it's shelter.

2. Transaction Fees Eat Housing Returns

Time is one cost of getting money out of real estate.

Equally important is the lack of liquidity and the onerous transaction fees. If you sell your house, you can kiss 5-6% of the price goodbye as fees to an agent.

On top of the expected months of waiting and agent costs, there are various fees plus transfer taxes and other hidden costs. It's not unheard of to pay 10%+ of a house's price to sell.

(And you likely are going to buy again, starting the whole cycle over!)

Let's talk about stocks again for a second. As long as the market is open, you can trade stocks basically instantly - or at least so fast (in most stocks!) you can't tell the difference.

As for the price of stock trades? With a company like M1 Finance you won't pay anything to trade.

3. You Probably Won't Be Diversified Without a Mortgage

For many people, their house makes up a majority of their net worth. For others, they've come to learn about paying off debt:

- Credit cards

- Student loans

- Car loans

- Personal loans

- And so-on.

If you've paid off your consumer debt recently, it's only natural to look at the largest debt you find yourself owing: your mortgage.

Here's the problem: if you recently had to pay off a number of debts, you probably don't have many assets.

If your house is the biggest thing you own I'll lay it out for you:

- You're making a concentrated bet on real estate

- *Residential real estate

- In your town

- Real estate on a specific neighborhood, on a specific street

- With specific neighbors, foliage, traffic patterns, etc

Get my point? If you don't, reread the first section about how your house isn't an investment.

House rich and cash poor isn't a great situation. Liquidity and maneuverability is worth a lot.

4. Mortgages Are Cheap

You can get a 30-year fixed mortgage with an interest rate below what people got on Treasuries in the 1970s: mortgage are very cheap, historically.

And, there's more - if you itemize, interest on up to $750,000 in a mortgage used to buy your house is deductible. Depending on your state and tax bracket, this could mean a reduction of up to 50% of the rate.

Yes, it's a lot of money and

5. Your IRA and 401(k) Have More Legal Protection

Have fewer than $1.3-$2.6 million in assets? Let me paint a scary picture for you:

Two neighbors each have a net worth of $1 million. They are both married and 40 years old. One owns his house outright, valued at $1,000,000. The other has $250,000 in equity in his house, and $750,000 between his 401(k) and IRAs.

They both are sued, and both have judgements of $2,000,000 against them. Both declare bankruptcy. What happens next?

Both neighbors are residents of California (look up your state). California lets most married couples exempt $100,000 from home equity in a bankruptcy. Neighbor A has $900,000 of assets at risk. Federally, you can exempt $1,362,800 per person. Neighbor 2 therefore only has $150,000 in equity at risk.

I'm not a lawyer and this is not legal advice. The law is complicated and never common sense - consult your own lawyer and financial adviser when discussing legal protection.

(These rules often don't apply if the government is the one asking for money. Oh, if you have that many assets, get umbrella insurance.)

Still, I'd rather be neighbor B in this situation - note he and his wife can shield a very solid amount of assets in the case of a bankruptcy. Did you know that retirement accounts and homes had such disparity in bankruptcy?

Don't Pay Off Your Mortgage

If you're fully diversified, aren't treating it as an investment, it's costing you too much, and you've already got $1.36 (or $2.72) million in retirement accounts it might be a good idea to pay off your mortgage.

If that doesn't describe you, it's not a good idea to pay off your mortgage early.