Leveraged ETFs are a time bomb in the portfolios of many investors. Unless you know exactly what they are and what they're doing you should avoid leveraged ETFs entirely.

Because of constant daily deleveraging and leveraging, you run into an issue known as the constant leverage trap. Unfortunately, the trap is paid for by your portfolio.

Thanks to our friend JT for his contribution to this post!

Leveraged ETF Problems & Leveraged ETF Decay

In theory, Leveraged ETFs seem like a great idea to many investors. They work by delivering some multiple of an index's return in their own return. They do it by either going long or going short that index.

So, for example, take the ETFs SSO and SDS:

- SSO - "ProShares Ultra S&P500". "The investment seeks daily investment results, before fees and expenses, which correspond to twice the daily performance of the S&P 500 Index."

- SDS - "ProShares UltraShort S&P500". "The investment seeks daily investment results, before fees and expenses, which correspond to twice (200%) the inverse (opposite) of the daily performance of the S&P 500."

These funds are supposed to deliver 2x return – in a bullish or bearish direction – of the S&P 500. In practice, look at this chart of SSO (blue), the S&P 500 (green) and SDS (red):

Even though the S&P 500 is up slightly, SSO did not match the returns of the two times the index. SDS fared even worse - losing more than 20% when the S&P 500 wasn't up anywhere close to 10%. Whoops!

What is the Constant Leverage Trap?

Here's the main problem with these funds: they are not meant to be held for longer than a day.The key word in the descriptions is "daily performance".

The ETFs attempt to maintain a daily leverage of 2x (or something else).

What you get is an automatic re-balancing problem. The long fund buys contracts and assets when prices increase, while the short fund does the opposite.

In a day when the market declines, the short fund is selling on a down day. Sell high & buy low is no recipe for success, especially when you're also paying a management fee.

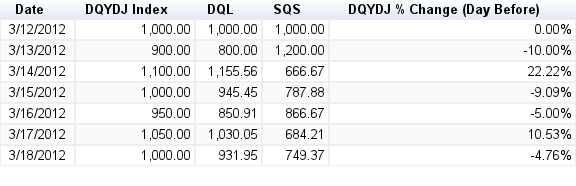

Ignoring a fee, how would that work with some random funds? Let's look at 3 random days and 2 random funds.

- DQL - goes 2x long the DQYDJ Index

- DQS - goes 2x short the DQYDJ Index

- Everything starts at 1,000.

Even though the market traded sideways over the 7 days in question, both the short and the long fund lost money.

What is the constant leverage trap?

Re-balancing assets will erode the value of your daily leveraged fund unless markets follow a very strong trend. To make what you think you'll make, markets would have to increase every day or decrease every day,

Markets have a generally positive drift rate, but truly strong trends of the type I'm describing are rare. Note that this analysis ignores the impact of management fees on the funds themselves.

Advanced Market Strategies: Shorting Leveraged ETF Pairs

I suppose I could also have named this section how to make money with the constant leverage trap. This section requires a disclaimer: in no way am I recommending this strategy. I'm just pointing out that the old line that 'if something is horrible to buy it must be great to sell'.

Do your own research, but consider shorting leveraged pairs.

We decided to cast our net further for an expert opinion and solicited some comments from JT:

Levered ETFs can be great...for the short-term. Otherwise, the decay eats investors alive. As for a pairs trade, it can definitely work in a simulated universe. I have open pairs shorted in my play portfolio at Fool.com where I've become one of the top 1% performing members just because of open shorts on levered funds.

In a real account, the ability to short a leveraged fund can be limiting. Borrowing shares of stock is not flat-rate; some require more or less money depending of course on supply and demand. It's entirely possible that it would cost you 50% or more per year to short a leveraged fund. (The first short-sellers in Groupon were reportedly paying as much as 90% per year to sell short - and it wasn't guaranteed to go down in value like leveraged ETFs are!)Can you make money with this strategy? Absolutely! But you'll have to have the confidence that you can acquire shares to short at a favorable rate. I'd leave it to the brain-heavy institutional investors who have more brainpower than I do when pricing their investments or lending shares to short-sellers.

This is essentially a volatility play, since you'll make money only if volatility in the future is higher than expectations (and thus decay happens faster than expected by traders lending shares to short-sellers.) Otherwise, the cost to short an ETF should be in line with expected decay given the current market volatility.The people who make the real money with levered exchange-traded products are the ETN issuers. Imagine how great it must be to sell a note at $100 and know that over time, the odds are that it will go to zero. The IPO of a new ETN is essentially free money for the issuer, with only minute, short-term risk. If you launch two levered ETNs going in either direction with roughly the same amount of investment interest, you'll laugh all the way to the bank!

For a more detailed description of the strategy, see this post on shorting leveraged pairs from blogging friend Darwin at Darwin's Finance.

More Comments on Leveraged ETFs

In this strategy, you would short sell the short and the long end of a pair. Set some sort of limit on the long side - remember markets can only fall to zero. (They can go as high as they like.)

Set your limit at a point where the opposite fund would have gone to zero. Also, reevaluate it often to avoid the problem described in this post!

If you really want to make money off these products - take JT's advice and start a financial company to issue these ETFs. The average investor should stay well away from these money traps... although it's possible there is a systemic risk building.

Want even more reason to avoid them? Read about the decline of $XIV, a short volatility fund.

Do you own any leveraged ETFs? How have they performed in your portfolio? Will you be changing your approach? Do you better understand the constant leverage trap?