Previously, we talked about the historical homeownership rate in the United States, with data back to the 1890s. Today, we'll discuss the 30 year mortgage's history and other innovations leading to the United States housing market's current status.

Even though we don't have the resolution to discuss every mortgage innovation, we can still point to historical changes. You'll be able to see (even at this level) how mortgage availability has affected the United States.

A Brief History of Mortgage Innovations Including the 30 Year Mortgage

We did some research on the origins of the modern mortgage... and it's pretty interesting.

Before the Great Depression, mortgages were completely privat. Homeowners would string refinances one after another, and mortgage terms were less than 5 years long.

It wasn't until 1934 that the Federal Housing Administration stepped in with an insurance program on mortgages, an amortization plan, and terms of 15-20 years. This hasn't changed much today: many mortgages are insured conforming to standardized programs - say, 30 years, fixed interest, 80% loan to value.

The FHA introduced other innovations:

- Quality requirements for insurance

- 10% and 20% down (from the previous ~50%).

While other Depression-era government programs were unpopular, the FHA's program became exceedingly popular. It featured submarket rates of 5% vs. prevailing interest rates around 12% at the time.

Undoubtedly, it also fueled the public's perspective that a mortgage is a generational commitment. You can draw a direct link from those 10, 15, and 20 year mortgages to the popular 30 year terms of today.

The Invention of Mortgage Insurance

If our first inflection point is around 1934, our second will be in the mid 1950s with the creation of mortgage insurance.

Even though the early Mortgage Insurance industry started in the 1880s, most all private mortgage insurance companies were bankrupted by the Great Depression. The FHA had an insurance program, but for substandard down payments there really wan't anything out there.

In 1957, the company The Mortgage Guaranty Insurance Company changed that.

They assumed risks on the first 20% of losses on a loan, allowing borrowers to put down less than the prevailing customary down payment of 20%.

Today, depending on the loan program you choose, you can put down less than 20% on a mortgage with insurance from various government, private, and quasi-government agencies.

So, to recap the major inventions that spurred homeownership in America:

- 1934 was when we first saw "modern" mortgages

- 1957 was the beginning of the PMI era

The Homeownership Rate and Mortgage Financing

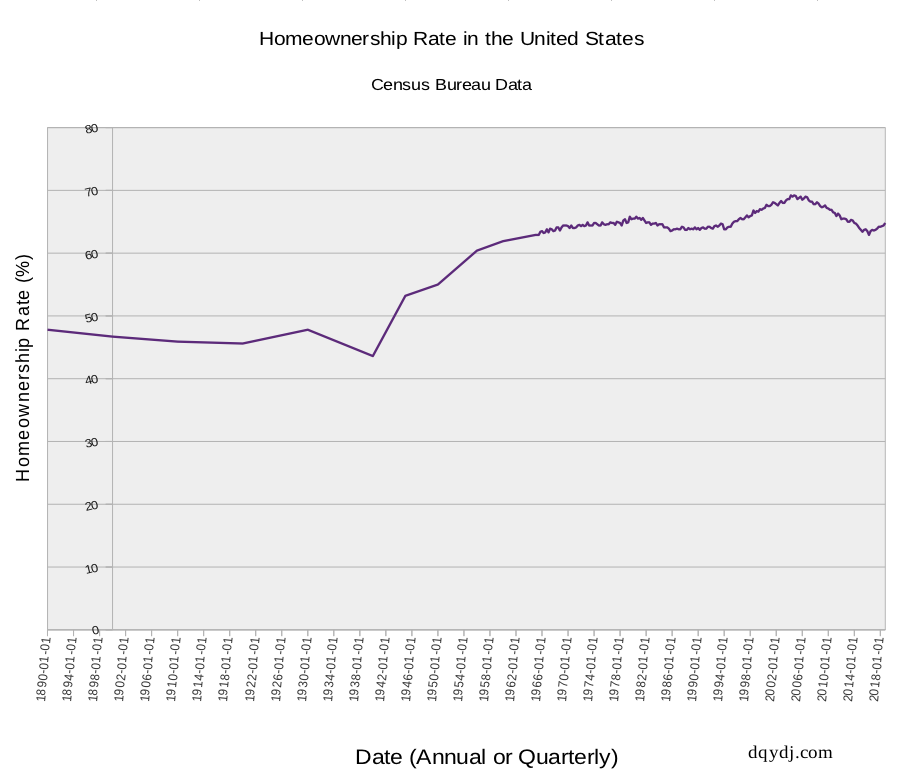

Here is the homeownership rate dating from 1890 until 2019, courtesy the Census Bureau. (We wrote up the story of this data here).

Number of Owner Occupied Homes with a Mortgage

Above, we've graphed the homeownership rate in the United States. However, this is ostensibly an article about mortgage innovations. That in mind, let's look at the proportion of homes financed with a mortgage.

| Date | Owner Occupied Homes with Mortgage |

| 01/01/2019 | 61.74% |

| 01/01/2018 | 61.93% |

| 01/01/2017 | 62.81% |

| 01/01/2016 | 63.04% |

| 01/01/2015 | 63.27% |

| 01/01/2014 | 63.76% |

| 01/01/2013 | 64.32% |

| 01/01/2012 | 65.74% |

| 01/01/2011 | 66.42% |

| 01/01/2010 | 67.23% |

| 01/01/2009 | 67.81% |

| 01/01/2008 | 68.43% |

| 01/01/2007 | 68.35% |

| 01/01/2006 | 68.23% |

| 01/01/2005 | 67.90% |

| 01/01/2000 | 64.48% |

| 01/01/1990 | 61.60% |

| 01/01/1980 | 60.66% |

| 01/01/1970 | 60.56% |

| 01/01/1960 | 56.77% |

| 01/01/1956 | 55.40% |

| 01/01/1950 | 43.97% |

| 01/01/1940 | 45.28% |

| 01/01/1920 | 39.84% |

| 01/01/1910 | 33.29% |

| 01/01/1900 | 32.02% |

| 01/01/1890 | 27.70% |

Sources on the History of the Mortgage and Mortgage Usage for Homes

To start, use Census Factfinder for the 2005+ ACS. Table is 'B25081'.

Then you need to tick through the 2001, 1991, 1981 Residential Finance Surveys.

Then revisit the Historical Statistics of the United States through 1970.

Conclusion

So, those charts look pretty similar, right?

Post hoc ergo propter hoc and all that, but it's tough to deny the link between access to mortgages and PMI and the homeownership rate in this country.

Note, too, that all of this increase in homeownership was in the midst of a massive growth in native born and immigration to the country.

How much do you think can be credited to the 30 year mortgage and other long dated loans? How about private mortgage insurance?